Die SRG schliesst das Betriebsjahr 2016 mit einem Überschuss von 25 Millionen Franken ab. Das Plus wäre allerdings nur halb so gross gewesen, wenn nicht 13 Millionen freigemacht worden wären durch eine vorzeitige Auflösung von Rückstellungen, wie die NZZ schreibt. Dieser Betrag wird eingesetzt im Zusammenhang mit der Senkung des technischen Zinssatzes der Pensionskasse. Der öffentliche Rundfunk stellte im Jahr 2013 auf das Beitragsprimat um und garantierte, bei einer Senkung des technischen Zinssatzes die entstehende Finanzlücke während fünf Jahren zu schliessen. Dafür setzte die SRG bereits 230 Millionen Franken ein, weshalb sie 2015 und 2012 mit tiefroten Zahlen abschloss.

April 8, 2017

US: The Unavoidable Pension Crisis

There is a really big crisis coming. Think about it this way.

There is a really big crisis coming. Think about it this way.

After 8 years and a 230% stock market advance the pension funds of Dallas, Chicago, and Houston are in severe trouble. But it isn’t just these municipalities that are in trouble, but also most of the public and private pensions that still operate in the country today.

Currently, many pension funds, like the one in Houston, are scrambling to slightly lower return rates, issue debt, raise taxes or increase contribution limits to fill some of the gaping holes of underfunded liabilities in their plans. The hope is such measures combined with an ongoing bull market, and increased participant contributions, will heal the plans in the future. This is not likely to be the case.

This problem is not something born of the last “financial crisis,” but rather the culmination of 20-plus years of financial mismanagement.

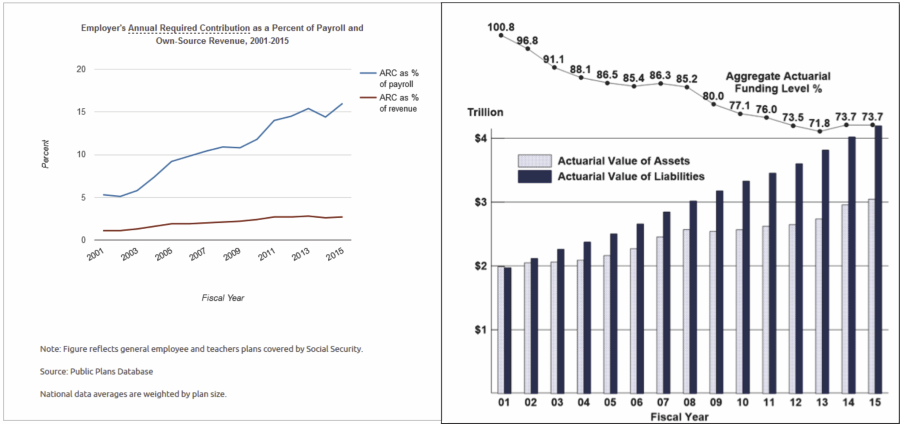

An April 2016 Moody’s analysis pegged the total 75-year unfunded liability for all state and local pension plans at $3.5 trillion. That’s the amount not covered by current fund assets, future expected contributions, and investment returns at assumed rates ranging from 3.7% to 4.1%. Another calculation from the American Enterprise Institute comes up with $5.2 trillion, presuming that long-term bond yields average 2.6%.

With employee contribution requirements extremely low, averaging about 15% of payroll, the need to stretch for higher rates of return have put pensions in a precarious position and increases the underfunded status of pensions.

{kind=link}